what goals to use in an incentive plan

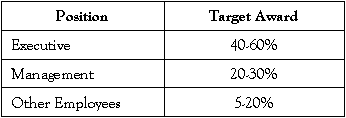

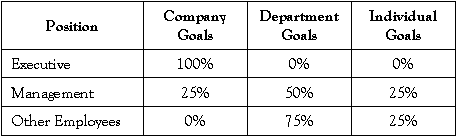

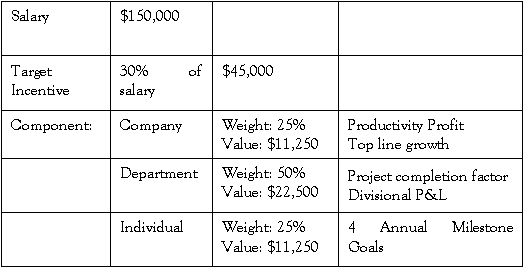

A successful incentive plan isn't doable unless information technology congenital on the right premise. Stated another way, well-nigh incentive plans neglect because they are built on a faulty premise. Company leaders create them believing they tin be used to touch employee behavior. When their program doesn't prompt the anticipated modify, those leaders claim it didn't "work" and go frustrated. They then change the programme metrics thinking that will solve the problem. But, if they started with the wrong premise, the new metrics only compound the trouble. So, let'southward solve this dilemma, shall we? To design a bonus or other brusque-term programme finer, you must start by correctly identifying the purpose of your offer. Sharing value with employees is a way to define the financial partnership you want to accept with them. Y'all are substantially inviting them to share your vision for the visitor and communicating the outcomes that need to be achieved to fulfill it. Further, through the manner you are paying them, you are identifying how they will participate in the value they aid create as they aid build the futurity company; in other words, how they will be rewarded for achieving the outcomes their role exists to produce. The premise, then, upon which an incentive plan should be congenital is value creation. It should grow out of a company philosophy which holds that employees volition share in the wealth multiple they help create. And as more value is created, more value-sharing can occur. And that is the term that should exist used to depict the plan the organization is creating--value-sharing. When you build a plan on a value-sharing premise, people are not rewarded for their behavior. They are rewarded for creating value. And the value creation that results in highest value-sharing should be that which almost aligns with shareholder interests. So, what might that exist? The Principal Focus Presumably, if you lead a concern, your primarily focus each year is profits. Your business concern growth depends upon it. What, then, should exist the principal mensurate upon which an incentive plan should be based? Yes, profit. This does not hateful y'all tin can't accept other metrics and measures. Only information technology does mean that profit should be primary. In other words, it doesn't affair how many other measures the company or section or private meets. If a certain turn a profit threshold is not achieved, incentives are not paid. This makes the development of other performance metrics easier not harder. Every measure out becomes issue based. Every bit a consequence, the cadre question in building metrics becomes: "Will this effect drive greater profits?" or "What outcome can this part produce that will increase profits?" If an outcome doesn't result in greater profits, and so that metric should probably be rejected or modified. And that leads to the other outcome that must exist addressed in defining measures and metrics. I Value-Sharing Philosophy, Two Performance Periods Yous should not develop an incentive plan that improves profits today at the expense of sustained growth. Those are considered "bad" profits. And they occur too often. They occur because business concern leaders unknowingly encourage them by offering incentives that are rooted in the wrong premise. Here'southward what I mean: A company sets upward an annual bonus program that maximizes payouts for achieving curt-term functioning goals. This compromises employee decision-making. They may stop upwards exploiting a client, vendor or other department in their visitor to enrich themselves while eroding long-term value creation in the process. Turn a profit is still generated, but it's bad profit. The answer to this problem is to think in terms of two performance periods when building an incentive plan. One is the next 12 months. Here, the focus is on achieving outcomes that meliorate revenue growth, expand margins or lower costs (or all three) but without damaging sustained growth. The second focuses on rewarding enduring performance—results that bulldoze business organization growth and increase shareholder value. This is accomplished by ensuring your employee "growth partners" are focused on outcomes that will improve business organization value (production development, acquisitions, new technology, expanded markets, etc.). Rewards, so, for short-term operation should exist tied to profits. And long-term rewards should be tied to business value increment. Why? Because they are correlated. You need profits to bulldoze growth. And employees are more probable to produce practiced profits if it works confronting their fiscal interest to think brusk-term. So, to summarize, the main metric for a short-term plan should be turn a profit. And long-term plan benefits should exist tied to a metric rooted in business value increase (which is actually but sustained profits). For both functioning periods, the role of the primary metric is to accomplish the post-obit: Remember, value-sharing is not initiated in an effort to change behavior or "motivate" employees, per se. Motivation is intrinsic and each employee will accept their own reasons to be committed to high performance. Notwithstanding, motivation is facilitated when employees' roles and tasks are aligned well with their unique abilities and are consistent with the purposes they want to serve or advance. Motivation is further engendered by a shared vision and values between the visitor and its workforce. On the other manus, if performance standards are not conspicuously divers and properly rewarded, an incentive program tin can potentially deflate the motivation of employees. This happens when a member of the workforce doesn't feel as though there is alignment betwixt his or her office and how rewards are earned. This creates frustration and disillusionment, ii conditions that are at odds with a positive focus and a high-operation culture. Two Core Approaches Once you accept established profit as the primary metric for your short-term plan, there are essentially two approaches you tin can take in constructing your plan. Ane is to base it solely on profits. The other is to place other key performance indicators (KPIs) you would similar to introduce in improver to the profit threshold. Let's wait at each. Profit-Based Allocation Under this approach, a company decides that it volition allocate a percentage of annual profits to employees. The award amount is divided among participants based on a pre-determined formula. Typically, payouts occur at year terminate, merely some companies prefer to make those payments quarterly. As indicated, the focus of this kind of program is solely on annual profits. As a result, the incentive value created tin be open ended (unlimited). This can be good or bad (more on that issue in a infinitesimal). The design of this kind of incentive is relatively unproblematic; all the same, it is essential that information technology exist accompanied past a stiff performance management organization. This is because in a turn a profit-based incentive environs, rewards are driven strictly by visitor operation, non private or department performance. As a issue, a separate management system needs to be in place to reinforce the outcomes that have to be achieved to drive the correct level of profits. The Profit-Based Allocation has some inherent dangers or drawbacks. This arroyo does not always create the consummate "line of sight" an arrangement wants reinforced past its compensation strategy. Too, because the program is centered solely on company performance, employee apathy tin can set in and morale issues tin arise. Consequently, if in that location is a lack of a strong performance management system in the organisation, this approach can be troublesome. With those dangers in listen, in a "best practices" framework, a Profit Based Allocation should address and/or account for the following issues: Targeted KPIs The theory behind the KPI approach is that improvements in the focus and execution of employees on the issues they are best positioned to impact volition lead, ultimately, to improvements in profits. A plan that uses KPIs can contain visitor, department or individual metrics—or all three. The value of the programme is typically capped, and its design can run from quite simple to very complex. What is essential in this approach is selecting the right metrics. This means you are going to place indicators that volition be used to mensurate performance in each area. For case, company metrics might be a combination of revenue growth and net income. Departmental indicators could be such things every bit comeback in visitor retention or an increase in the collection rate on accounts receivable. Individual metrics would be tied to personal operation goals and productivity factors. Here are some examples of company and department indicators that we take seen used in the past finer. Of course, their application will vary depending on industry and other factors. In our experience, KPI approaches work best if they contain the post-obit elements. Range of Incentive Attractive target incentives should be established for each position. In general, growing companies size their incentives in a range of 25% to 100% of salaries for senior executives. Of course, lower ranges are set for the other tiers. Sample Components of Incentive Calculation Next, the company should decide how much of an individual's incentive will be based on (a) company operation, (b) department/division operation, and (c) individual functioning. Sample Key Determinants (Drivers) Company Drivers Department Drivers Individual Drivers Pre-Decision The incentive components should be established and communicated in advance of the incentive catamenia (typically annually). The employee should be able to identify and understand the exact requirements associated with achieving his or her target incentive. For example, an incentive construction for a Department Caput might exist communicated as follows: Incentive targets may exist tiered to eliminate an "all or zippo" consequence. Commonly, three to v tiers are recommended. The payout results at each tier should be significantly greater than the preceding tier. Frequently, the plan grid (run across beneath) can help produce this "tiering" effect. Executives are often provided with clear measurement grids to help balance not-correlated or complementary goals. Below is an example that could be used for a company-wide filigree. There is no i perfect solution to designing an incentive program that will be effective for every visitor. As a event, the way a visitor approaches the ideal is to understand best do standards and frameworks and then work within that construction to customize indicators, measures and metrics that are suitable for your business. The selection of the type of incentive plan and its associated metrics should exist based a company's culture, business model and goals. Here we take introduced two effective approaches to developing incentive plan indicators. But regardless of the design you select, outset with the right premise and utilize profit as your chief metric. Learn More Nigh the Purpose of Incentive Compensation

The dangers with the KPI approach can include the post-obit (among other things):

The determination of this weighting is predicated on the degree of impact each person (position) is accounted to possess relative to the associated result area.

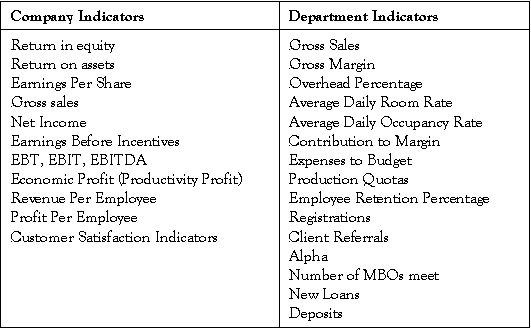

Metrics to consider for company performance might include:

Departmental metrics might include:

Key Performance Indicators (KPIs) designed to measure individual performance autumn into two categories: difficult measurements and soft measurements. Hard measurements include specific metrics calculated to reverberate on the directly control of the participant. An example of a soft measurement would exist the "completion of a specific project by a specific date."

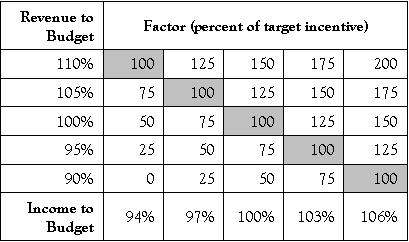

Tiered Awards  In Determination

In Determination

courterwereemild51.blogspot.com

Source: https://blog.vladvisors.com/blog/selecting-the-right-performance-measures-for-your-incentive-plan

0 Response to "what goals to use in an incentive plan"

Post a Comment